All Categories

Featured

Table of Contents

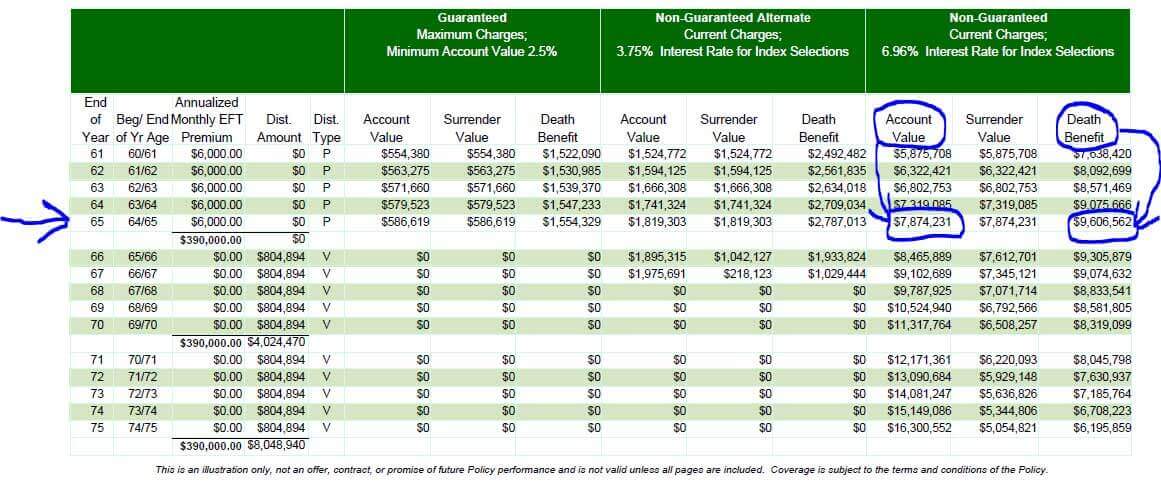

Indexed universal life policies use a minimal surefire passion price, also known as a passion attributing flooring, which decreases market losses. Say your cash money worth sheds 8%.

A IUL is a long-term life insurance coverage policy that obtains from the properties of a global life insurance plan. Unlike universal life, your cash worth grows based on the performance of market indexes such as the S&P 500 or Nasdaq.

What makes IUL different from other plans is that a section of the premium repayment goes right into annual renewable-term life insurance. Term life insurance policy, additionally recognized as pure life insurance coverage, assurances death benefit settlement.

An IUL plan may be the best choice for a client if they are trying to find a long-lasting insurance coverage product that builds riches over the life insurance term. This is because it provides prospective for development and additionally preserves the a lot of value in an unsteady market. For those that have substantial properties or riches in up-front financial investments, IUL insurance policy will certainly be a terrific wide range administration device, especially if someone wants a tax-free retirement.

What is the process for getting Indexed Universal Life Plans?

In contrast to other plans like variable global life insurance, it is much less dangerous. When it comes to taking treatment of beneficiaries and handling wide range, below are some of the top factors that a person might pick to choose an IUL insurance coverage policy: The money value that can build up due to the rate of interest paid does not count toward profits.

This indicates a customer can use their insurance policy payment as opposed to dipping into their social safety cash prior to they prepare to do so. Each policy must be customized to the client's individual demands, especially if they are handling substantial possessions. The policyholder and the agent can choose the amount of danger they think about to be appropriate for their needs.

IUL is a general conveniently adjustable plan. As a result of the rate of interest of global life insurance policy plans, the rate of return that a customer can potentially get is greater than various other insurance policy protection. This is since the proprietor and the agent can utilize call choices to boost possible returns.

Who offers Indexed Universal Life Death Benefit?

Insurance policy holders may be drawn in to an IUL policy because they do not pay resources gains on the extra money value of the insurance plan. This can be contrasted to other policies that need taxes be paid on any kind of cash that is gotten. This suggests there's a cash money possession that can be gotten at any moment, and the life insurance coverage policyholder would certainly not have to stress over paying taxes on the withdrawal.

While there are several different benefits for an insurance policy holder to select this type of life insurance coverage, it's not for everybody. It is essential to allow the customer know both sides of the coin. Here are some of the most vital points to encourage a customer to take into account prior to selecting this choice: There are caps on the returns an insurance policy holder can get.

The most effective alternative relies on the client's risk tolerance - Indexed Universal Life for retirement income. While the charges related to an IUL insurance coverage deserve it for some consumers, it is necessary to be ahead of time with them regarding the expenses. There are premium expense charges and other administrative fees that can begin to accumulate

No ensured passion rateSome various other insurance coverage plans supply an interest rate that is ensured. This is not the instance for IUL insurance policy.

Why should I have Long-term Indexed Universal Life Benefits?

Consult your tax obligation, legal, or accountancy expert regarding your private scenario. 3 An Indexed Universal Life (IUL) policy is not thought about a safety. Costs and death advantage types are flexible. It's attributing rate is based on the efficiency of a supply index with a cap rate (i.e. 10%), a flooring (i.e.

8 Irreversible life insurance policy contains 2 types: whole life and global life. Cash money worth expands in a participating entire life plan via dividends, which are declared annually by the firm's board of directors and are not ensured. Money worth grows in a global life plan through credited rate of interest and lowered insurance policy expenses.

Who offers flexible High Cash Value Iul plans?

No issue just how well you prepare for the future, there are events in life, both anticipated and unforeseen, that can impact the financial health of you and your liked ones. That's a factor for life insurance policy.

Things like potential tax boosts, inflation, financial emergencies, and preparing for occasions like college, retired life, and even wedding celebrations. Some kinds of life insurance coverage can assist with these and various other worries too, such as indexed global life insurance, or simply IUL. With IUL, your plan can be a funds, because it has the potential to build value gradually.

You can choose to receive indexed interest. An index might affect your interest credited, you can not spend or straight get involved in an index. Right here, your policy tracks, yet is not in fact purchased, an exterior market index like the S&P 500 Index. This theoretical example is offered illustrative objectives only.

Fees and costs might decrease policy worths. You can additionally choose to obtain fixed interest, one collection predictable interest price month after month, no issue the market.

Who offers Iul Policy?

That leaves more in your plan to potentially keep growing over time. Down the road, you can access any readily available cash value via plan loans or withdrawals.

{kind=link}

Table of Contents

Latest Posts

Minnesota Life Iul

Seguros Universal Insurance

What Is Group Universal Life

More

Latest Posts

Minnesota Life Iul

Seguros Universal Insurance

What Is Group Universal Life